CONSUMER RIGHTS LAW FIRM SERVING CLIENTS IN CHICAGO, ILLINOIS, AND NATIONWIDE

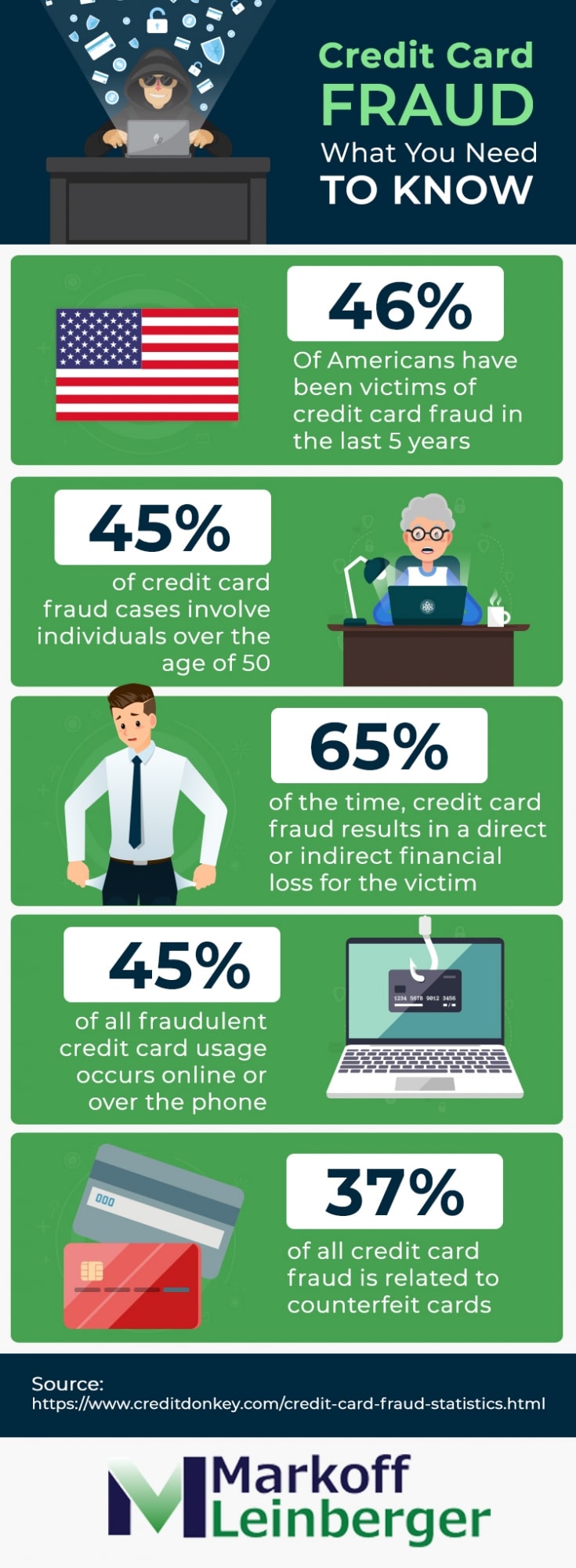

Credit card fraud is unfortunately fairly common, and can cause devastating damage to your finances and creditworthiness if you become a victim. If you notice anything unusual on your credit card statement or credit report, don't wait to hire an experienced consumer fraud lawyer to help you repair your finances before it's too late. In addition, if you notice that a merchant has not truncated your card number or expiration date on a receipt, you may be entitled to damages. See some of our recent credit card fraud settlements to get an idea of what kind of results we get.

The credit card fraud attorneys at Markoff Leinberger have years of experience helping consumers fight big credit card and credit reporting companies. Contact us at {tel} for a free case evaluation.

Credit Card Fraud Tactics

Some credit card companies resort to fraudulent and deceptive practices in order to increase their profits. Unfortunately, unsuspecting consumers can easily fall victim to these practices. However, if you notice something seems wrong about your credit card statement, you have the ability to fight back.

Some common credit card fraud tactics include:

- Hidden fees: Excessive fees for cash advances, balance transfers, and other cash transactions are often buried in the fine print of card member agreements.

- Late fees: Under the Credit Card Responsibility and Disclosure Act (also called the CARD Act) of 2009, first time late fees are capped at $25. If you are late more than once in a 6 month period, however, you may be charged more. If you were late only once and were charged more than $25, contact us.

- Masked APRs: Many credit card companies lure in new customers with low introductory APRs that are only short-term rates masking a higher regular APR. Under the CARD Act, significant changes in account terms must have at least 45 days advance notice.

- Not crediting past payments: Credit card companies will sometimes fail to record overdue payments so that they can fraudulently collect additional fees.

- Double cycle billing: Under the CARD Act, credit card companies may no longer calculate interest from the previous billing cycle. Interest charges must be based on the current cycle, in order to protect cardholders from extra charges even though they paid off their balance.

Unscrupulous merchants or thieves may also commit credit card fraud. Some of the most common examples include:

- Double charging: Whether by accident or intentional, double charging for a purchase is a fairly common occurrence. Always check your statements to make sure your charges are correct.

- Unknown charges: If you see charges on your statement for purchases that you never made, your card may have been compromised.

Credit Reporting Fraud

Most people don't pay much attention to their credit report, until the time comes that they want to purchase a home or lease a new car, and they suddenly find that they don't qualify for a good loan or a favorable interest rate.

Bad credit can affect your life in many ways, from purchasing a house to qualifying for a cell phone plan. It can even bar you from landing a job - some companies require credit checks before hiring. This is why it's so important to keep an eye on your credit score, and immediately investigate if anything seems incorrect.

There are three major credit reporting companies that keep records of all your credit transactions:

- Equifax

- TransUnion

- Experian

Creditors provide information to these companies on a daily basis, and with so many transactions, the potential for error is high. Every piece of negative information that a creditor provides about you goes on your credit report, affecting your creditworthiness.

What Can Cause Your Credit Report To Suffer?

Your credit report is a means to show how well you manage credit. These reports take into account such information as:

- How long you have held various credit accounts

- Your history of on-time and late payments

- Your total credit balances

- How many payments you have missed

If you hold a high balance or consistently miss or are late with payments, this negatively affects your credit score. If you are a victim of credit card fraud, this can wreak havoc with your credit score. In addition, if a credit agency makes a mistake on your report, this can also affect you negatively.

Your Rights Under The Fair Credit Reporting Act

Under the Fair Credit Reporting Act, your rights include:

- One free copy of your credit report per year

- The right to request that inaccurate information be corrected

- Negative information should be removed after 7 years (10 in the case of bankruptcy)

- You can sue credit reporting agencies and creditors who supply inaccurate information

- If you have a dispute that cannot be resolved satisfactorily, you can include an explanation on your report

- If inaccurate information cannot be verified, it should be removed

We recommend keeping a close eye on your credit report for any inaccuracies or potentially credit-damaging information that should not be on it.

The Credit Repair Organizations Act

When people accumulate a lot of debt, it can feel overwhelming and like they'll never get out of it. This paves the way for predatory credit repair organizations who offer to help repair your credit, but end up just taking your money. The Credit Repair Organizations Act (CROA) aims to protect consumers from these predatory companies.

Under CROA, credit repair companies are prohibited from:

- Asking for pre-payment for services

- Lying to creditors (or advising you to lie to creditors) about your credit history

- Attempting to change your identity

- Offering a "guarantee" to remove negative credit information

- Misrepresenting services provided

In addition to the above, CROA requires that credit repair agencies provide contracts in writing, and consumers are allowed to cancel their contracts within three days. These rights cannot be waived by consumers, even if language in a contract suggests otherwise.

If you believe you have been a victim of an unscrupulous credit repair organization, contact the credit repair attorneys at Markoff Leinberger for a free consultation to see if you may be entitled to compensation.

Schedule Your Free Credit Card Or Credit Report Fraud Consultation

If you have fallen victim to credit card fraud, credit reporting fraud, or a fraudulent credit repair company, contact the experienced Chicago consumer law attorneys at Markoff Leinberger today. Call 312-726-4162 to schedule your free consultation.

We serve clients in Chicago, Illinois and nationwide.